Duration matching between a bank’s deposits and asset portfolio is the primary focus for Asset Liability Management Committees (“ALCO”) as they manage their balance sheet. Deposit duration assumptions have been tested in recent years as interest rates have risen rapidly and technology has enabled deposits to move more quickly and with less predictably.

Understanding the duration of deposits becomes even more difficult if a bank’s deposit base is volatile, concentrated, and uninsured. Volatile deposits tend to have no predictable duration and are likely to run off during market uncertainty. A highly concentrated and uninsured deposit base can potentially lead to bank runs as we have seen recently with several institutions. One way ALCOs can protect against deposit runoff or a potential bank run is to hold a larger cash or liquid security buffer, but this limits their ability to allocate funds to higher-yielding asset classes. This results in a performance drag on a bank’s asset portfolio, i.e. “deposit drag” [1].

Faced with deposit uncertainty, we’ve even seen institutions move to shed less valuable deposits in recent weeks to recalibrate their balance sheet. However, ALCOs do have tools at their disposal to reduce deposit drag today, other than just turning away depositors. One solution is to engage in a reciprocal or sweep program, which allows banks to reduce the amount of uninsured and unwanted deposits as well as diversify their deposit base. Banks, however, need more alternatives. Specifically, banks need to be able to precisely calculate the quality of a deposit to understand its duration, its corresponding collateral needs and resulting “drag”, above and beyond the analysis they are able to do today. Technology can help here by potentially analyzing a bank’s deposit base down to the account level and incorporating a variety of customer and market factors. Better deposit products, combined with tech-driven insights to analyze the duration of a bank’s deposit base, will enable ALCOs to reduce deposit drag in the future. With a more diversified deposit base and accurate insights, ALCOs can reduce their cash buffer and improve performance with more confidence.

[1] In a previous newsletter, we spoke about “collateral drag”, the opportunity cost of potential return on assets when posting collateral.

Best,

Adam and the ModernFi Team

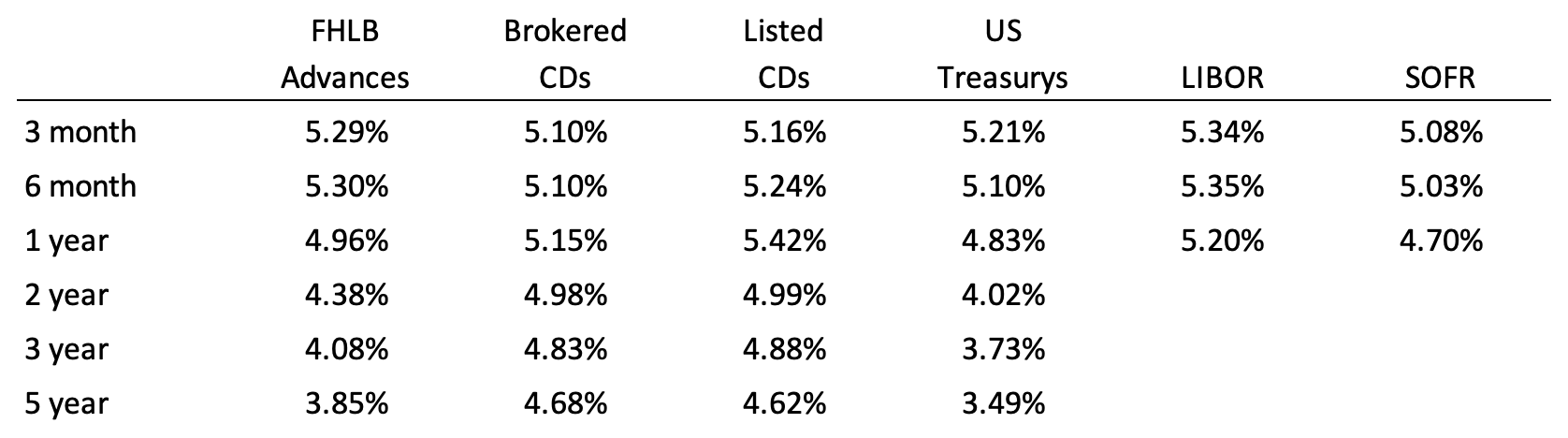

Current rates

Change from two weeks ago

Sources: FHLB Advances are an average of FHLB Boston, FHLB Chicago, and FHLB Des Moines. Brokered CDs are an average of Fidelity and Vanguard. Listed CDs provided by National CD Rateline. US Treasurys and LIBOR provided by WSJ. SOFR provided by CME.

Disclosures:

All information contained herein is for informational purposes and should not be construed as investment advice. It does not constitute an offer, solicitation or recommendation to purchase any security, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. Past performance does not guarantee future results. The information contained herein is for institutional use only.

ModernFi Advisers LLC (ModernFi) is not a bank, nor does it offer bank deposits and its services are not guaranteed or insured by the FDIC; ModernFi allocates funds to banks that are FDIC members. ModernFi is an investment adviser registered with the United States Securities and Exchange Commission (SEC). For more information regarding the firm, please see its Form ADV on file with the SEC through the Investment Adviser Public Disclosure website. Registration with the SEC does not imply a particular level of skill or training.

Certain information contained herein has been obtained from third party sources and such information has not been independently verified by ModernFi. No representation, warranty, or undertaking, expressed or implied, is given to the accuracy or completeness of such information by ModernFi or any other person. While such sources are believed to be reliable, ModernFi does not assume any responsibility for the accuracy or completeness of such information. ModernFi does not undertake any obligation to update the information contained herein as of any future date.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

Except where otherwise indicated, the information contained in this communication is based on matters as they exist as of the date of preparation of such material and not as of the date of distribution or any future date. Recipients should not rely on this material in making any future investment decision.

| A guest post by

|