The End of the Bank Term Funding Program and Increased Pressure on FHLB Advances

February 21, 2024 | ModernFi Insights

The Bank Term Funding Program (BTFP) will wind down in a couple of weeks on March 11, ending the lending program that the Fed launched in the aftermath of SVB. The Program, which offers loans of up to one year to depository institutions, was established to alleviate stress in the system. By valuing collateral such as Treasurys at par, the Program aimed to mitigate the potential of fire sales.

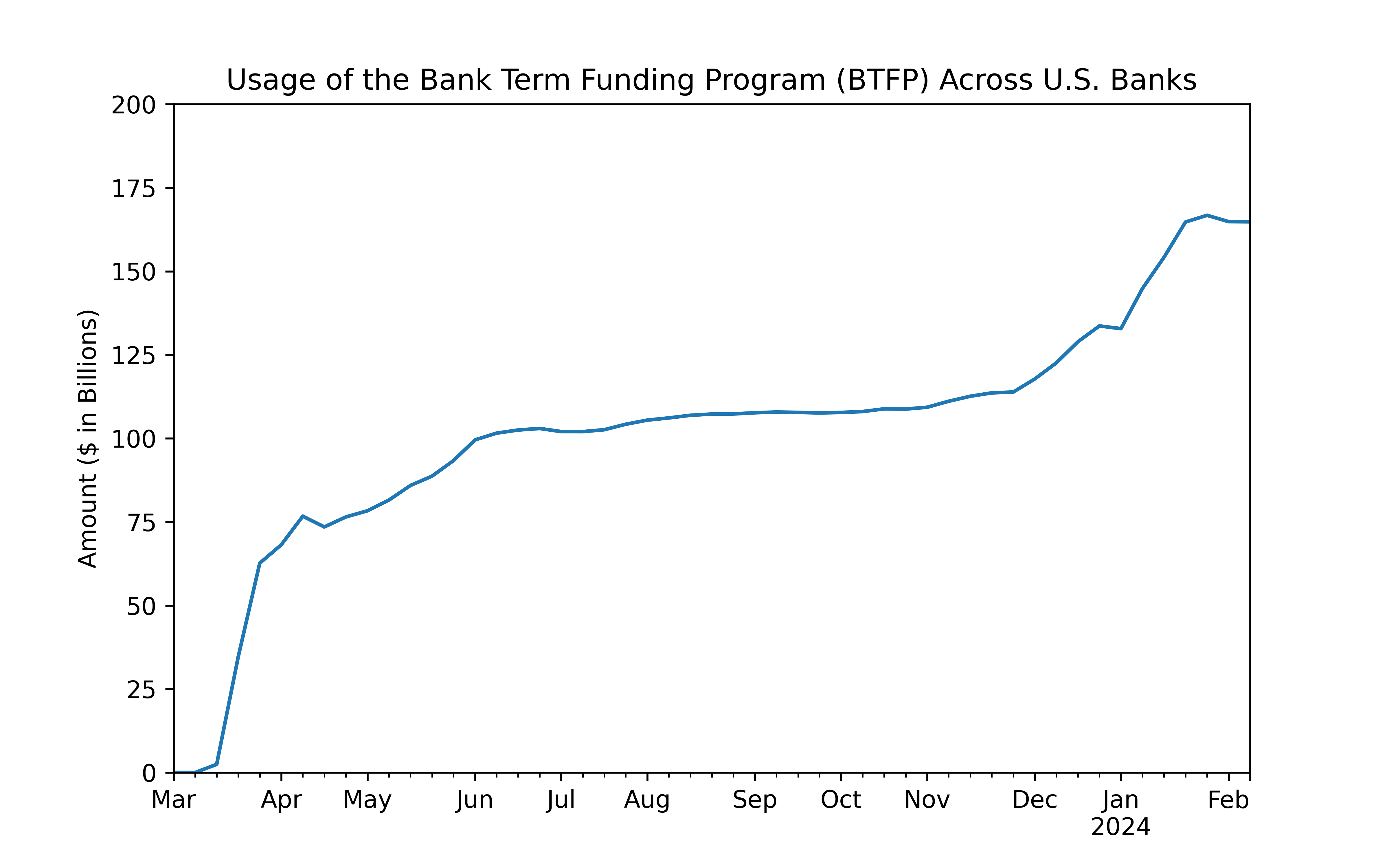

The Program was popular immediately after SVB, quickly growing to $62bn in loans three weeks after it was launched. Interestingly, it has remained a popular funding mechanism, with outstanding loans growing steadily to $165bn. The staying power of the Program indicates that it’s a favorable funding source, and some institutions are likely utilizing it as such (not only to mitigate stress). When the Program ends in a couple of weeks, those institutions will have to turn elsewhere for their funding. The likely alternative sources will be FHLB Advances and brokered CD markets.

Notably, FHLB Advances have also come under pressure in recent months. Advances are ideally supposed to “serve as a funding source for a variety of mortgage products, including those focused on very low- and low- and moderate-income households” (FDIC). However, due to their flexibility, availability, and cost, Advances are often tapped as just another funding source, and, as a result, they have grown to $805bn outstanding. This has led several voices to criticize the system and push for reform. If FHLB Advances are restricted, we would expect to see significant increases in brokered CD usage and increased pressure in funding markets in general.

With BTFP ending and FHLB under pressure, there’s lots to look out for over the coming months. In general, ensuring that our depository institutions have ready access to a diversity of available, flexible, stable, and cost-effective funding sources is paramount to the safety and soundness of the ecosystem.

Best,

The ModernFi Team

Current rates

Change from two weeks ago

Sources: FHLB Advances are an average of FHLB Boston, FHLB Chicago, and FHLB Des Moines. Brokered CDs are an average of Fidelity and Vanguard. Listed CDs provided by National CD Rateline. US Treasurys provided by WSJ. SOFR provided by Chatham Financial.

BTFP and FHLB data provided by fred.stlouisfed.org