In our previous newsletter, we briefly touched on how banks use alternative funding sources such as FHLB Advances to fill liquidity gaps. FHLB Advances are a powerful tool for ALCOs that provide both immediacy and transparency. Through an Advance, banks have same-day access to funds for immediate cash needs and can easily understand the cost and term of such funding. Advances, however, are a secured loan and may require additional collateral to be pledged if borrowing needs exceed the blanket lien.

Pledging additional collateral produces two strains on a bank: 1) the requirement to process collateral, and 2) a performance drag on a bank’s asset portfolio. A bank typically needs a team and processes in place to ensure that it is meeting FHLB’s collateral eligibility requirements and concentration limits. In addition, collateral haircuts — the amount at which FHLB values the collateral — make lower-return asset classes such as U.S. government or agency securities more favorable to pledge as collateral. As result, there is an opportunity cost, or “collateral drag”, of potential return on assets as Advances limit a bank from allocating funds to higher-performing asset classes.

In contrast, sourcing funding through deposits does not require collateral and does not produce collateral drag on a bank’s portfolio. Traditional means of sourcing deposits such as physical branches, digital banking, and deposit brokers do not provide the same level of immediacy and transparency as FHLB, limiting a bank’s ability to precisely fill liquidity gaps. Deposit networks, however, have the infrastructure to act in a similar capacity as FHLB, but traditional networks tend to transact via phone, email, and blind auctions. ModernFi has introduced a new deposit network model using modern technology and efficient operations to bring same-day or next-day deposit funding to banks. In the words of one of our partners, ModernFi’s solution acts like the “FHLB for deposits”.

While solutions like ModernFi increase funding efficiency for banks, an institution should never rely on one funding source. As we have learned time and time again, including from SVB, banks should have a diversity of funding sources on tap – a mixture of deposits from different customer types and in different deposit products, Advances, and ModernFi.

Best,

Adam and the ModernFi Team

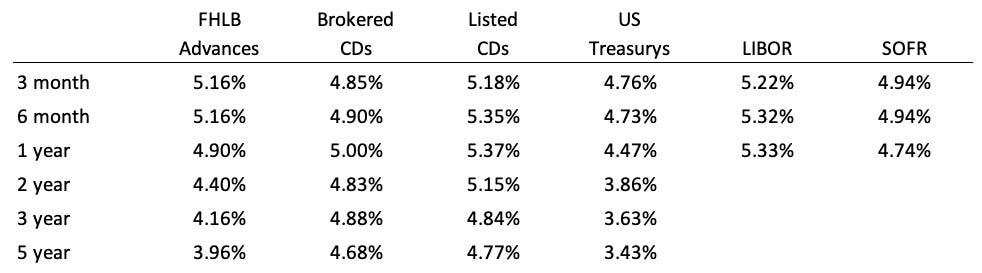

Current rates

Change from one week ago

Sources: FHLB Advances are an average of FHLB Boston, FHLB Chicago, and FHLB Des Moines. Brokered CDs are an average of Fidelity and Vanguard. Listed CDs provided by National CD Rateline. US Treasurys and LIBOR provided by WSJ. SOFR provided by CME.

Disclosures:

All information contained herein is for informational purposes and should not be construed as investment advice. It does not constitute an offer, solicitation or recommendation to purchase any security, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. Past performance does not guarantee future results. The information contained herein is for institutional use only.

ModernFi Advisers LLC (ModernFi) is not a bank, nor does it offer bank deposits and its services are not guaranteed or insured by the FDIC; ModernFi allocates funds to banks that are FDIC members. ModernFi is an investment adviser registered with the United States Securities and Exchange Commission (SEC). For more information regarding the firm, please see its Form ADV on file with the SEC through the Investment Adviser Public Disclosure website. Registration with the SEC does not imply a particular level of skill or training.

Certain information contained herein has been obtained from third party sources and such information has not been independently verified by ModernFi. No representation, warranty, or undertaking, expressed or implied, is given to the accuracy or completeness of such information by ModernFi or any other person. While such sources are believed to be reliable, ModernFi does not assume any responsibility for the accuracy or completeness of such information. ModernFi does not undertake any obligation to update the information contained herein as of any future date.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

Except where otherwise indicated, the information contained in this communication is based on matters as they exist as of the date of preparation of such material and not as of the date of distribution or any future date. Recipients should not rely on this material in making any future investment decision.

| A guest post by

|